Life insurance trusts are typically funded only with life insurance. It is not common to include other income-producing assets in the trust. Life insurance is kept separate from income-producing assets in trust because any income would be taxable to the grantor. The grantor of an ILIT typically doesn't want to create a trust that generates income-tax consequences for the grantor.

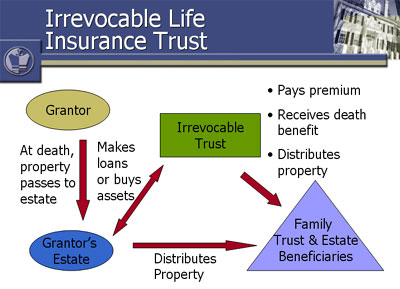

The appeal of an irrevocable life insurance trust is that, if properly arranged, the death proceeds of the policy are kept out of the insured's estate. The irrevocable life insurance trust can be considered a double winner in that, not only are the death proceeds outside the insured's estate, but the proceeds can be available to meet estate liquidity needs. However, any proceeds used for the benefit of the decedent's estate would be recognized as estate assets, unless they are used to purchase estate assets or loaned to the estate.

Detailed information regarding irrevocable life insurance trusts and their uses is available in the Estate Planning Adviser's Guide (Form 2450).

Copyright ONFS. Taken from ESTATEPLANNING PowerPoint Presentation, downloadable through ON-Net.

Ohio National is not affiliated with, nor does it endorse or sponsor, any particular prospecting, marketing or selling system.