During the Accumulation Phase

Tax Deferral

With a non-qualified deferred annuity, the single payment or periodic payments consist of money on which the annuitant has already paid income taxes. The interest (fixed annuities) or earnings (variable annuities) of these deposits is not currently taxed. Instead, taxation is deferred to a future date when the interest or earnings are actually withdrawn from the contract. Deferred annuities are one of the few investments still available that enjoy such tax-favored treatment.

Tax deferral is a powerful sales tool. The fact is that the more money is at work, the faster assets can grow. With a deferred annuity, you can bring the power of tax deferral to your prospects and clients. This power can be illustrated by comparing a tax-deferred investment, such as a deferred annuity, with a taxable investment, such as a CD.

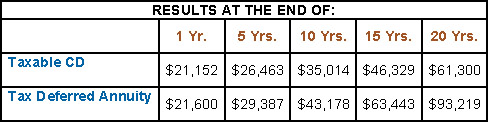

The illustration that follows is based on $20,000 invested in a deferred annuity and $20,000 in vested in a CD, with both earning 8%. The CD earnings are taxed each year as received, assuming a 28% tax bracket.

For longer-term wealth accumulation purposes, the deferred annuity is clearly superior, providing almost $32,000 more after 20 years. Although the earnings inside the annuity are subject to income tax when withdrawn, at the clients' then current tax bracket, the balance of the annuity not withdrawn would continue to grow on a tax-deferred basis. This enables the client to limit the amount of taxable income to only the amount withdrawn.

Ohio National is not affiliated with, nor does it endorse or sponsor, any particular prospecting, marketing or selling system.