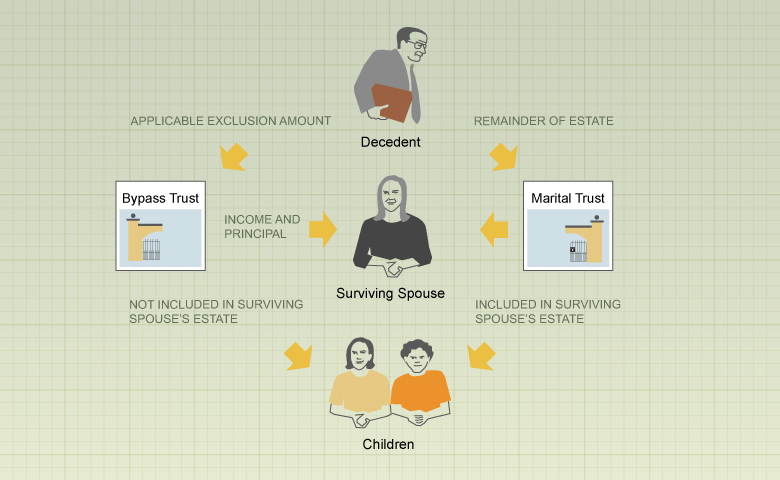

The decedent provides for a portion of his estate to be placed in a bypass trust, often equal to the applicable exclusion amount for the year of death.

The remainder of the estate is given outright to the surviving spouse or placed in a marital trust.

Income and principal from the bypass trust can be paid to the spouse during his or her lifetime.

At the surviving spouse's death, the children receive the property from both trusts, but the property in the bypass trust is not included in the surviving spouse's gross estate.

![]() View or print a high-quality version of this graphic (requires Adobe Acrobat Reader).

View or print a high-quality version of this graphic (requires Adobe Acrobat Reader).

![]()

Copyright ![]() 2016, Pentera Group, Inc., 921 East 86th Street, Suite 100, Indianapolis, Indiana 46240. All rights reserved.

2016, Pentera Group, Inc., 921 East 86th Street, Suite 100, Indianapolis, Indiana 46240. All rights reserved.

This service is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that neither the publisher nor any of its licensees or their distributees intend to, or are engaged in, rendering legal, accounting, or tax advice. If legal or tax advice or other expert assistance is required, the services of a competent professional should be sought.

While the publisher has been diligent in attempting to provide accurate information, the accuracy of the information cannot be guaranteed. Laws and regulations change frequently, and are subject to differing legal interpretations. Accordingly, neither the publisher nor any of its licensees or their distributees shall be liable for any loss or damage caused, or alleged to have been caused, by the use of or reliance upon this service.