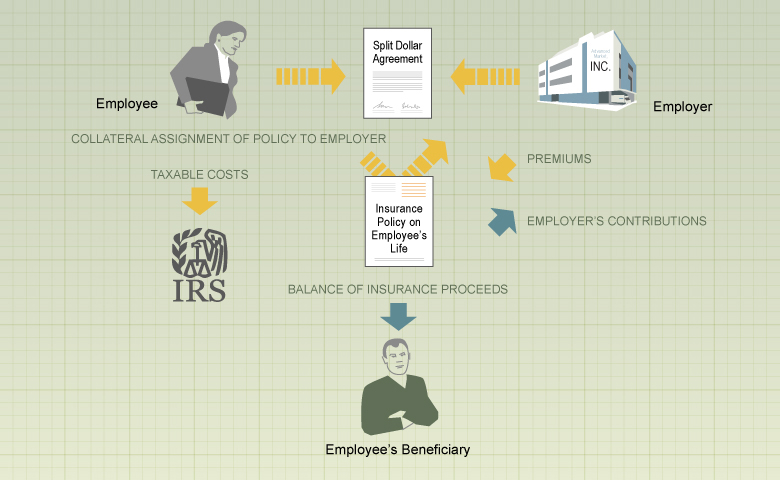

The employee owns the policy and collaterally assigns it to the employer.

The employer pays all of the premiums.

The employee includes the taxable costs of the split-dollar arrangement in gross income.

At the employee's death, the employer recovers its total premiums paid or the cash value, depending on the arrangement. The balance of the proceeds are paid to the employee's beneficiary.

![]() View or print a high-quality version of this graphic (requires Adobe Acrobat Reader).

View or print a high-quality version of this graphic (requires Adobe Acrobat Reader).

![]()

Copyright ![]() 2016, Pentera Group, Inc., 921 East 86th Street, Suite 100, Indianapolis, Indiana 46240. All rights reserved.

2016, Pentera Group, Inc., 921 East 86th Street, Suite 100, Indianapolis, Indiana 46240. All rights reserved.

This service is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that neither the publisher nor any of its licensees or their distributees intend to, or are engaged in, rendering legal, accounting, or tax advice. If legal or tax advice or other expert assistance is required, the services of a competent professional should be sought.

While the publisher has been diligent in attempting to provide accurate information, the accuracy of the information cannot be guaranteed. Laws and regulations change frequently, and are subject to differing legal interpretations. Accordingly, neither the publisher nor any of its licensees or their distributees shall be liable for any loss or damage caused, or alleged to have been caused, by the use of or reliance upon this service.